Research: A-brands, in the face of the own private label brand tsunami

- DRC Discount Retail Consulting GmbH

- Mar 18, 2023

- 7 min read

From time to time Promarca convenes an event where it denounces the scarce access that Spanish consumers have to the "manufacturer brands" on the shelves of leading chains such as Mercadona or Lidl; without much success, according to the constant growth of the distribution brand (MDD) or private labels (PL), even among the most loyal and aware retailers. High inflation and the loss of purchasing power of the shopper play against it.

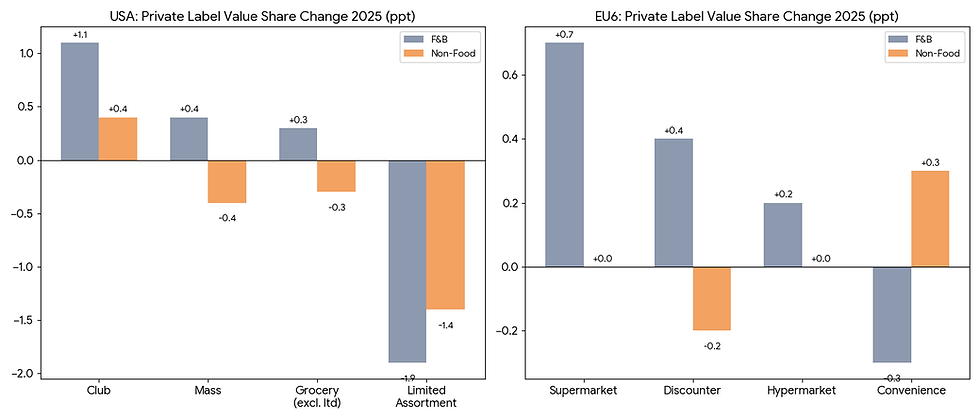

Promarca has organized a conference under the title "Present and future challenges of mass consumption", where experts in the food chain have spoken of the "challenges facing the sector", although, in reality, it could well have been titled "Manufacturer brands, before the tsunami of the PL". And it is that the increase in inflation (and the loss of purchasing power) has caused distribution, in a generalized way, has facilitated its customers access to low-price products focused on the most basic needs. Thus, the own brand has gained a new and strong momentum, turning Spain into the European paradise of private labels. The event aimed to raise awareness among different stakeholders of the negative effects that large retailers have on society, basing their commercial offer on a short assortment where lower-cost own brands predominate. "Competition almost exclusively based on prices creates a vicious circle: low cost wages, low cost taxes and general impoverishment," warns Ignacio Larracoechea. "The current situation is an attack on choice." "40% miss brands," he continues. The truth is that in the last ten years the presence of brands has been reduced by 24%, creating an extremely complex board for them where it becomes increasingly difficult to reference innovation. "Manufacturer brands generate ten times more added value than distribution brands," argues Larracoechea. BRANDED ASSORTMENT SHRINKS IN MOST CHAINS César Valencoso, Consumer Insights Director of Kantar Worldpanel, has spoken of "consumer freedom of choice" starting with a premise: wider assortments better meet the needs of different consumers. Since unlimited assortment is not viable, there is a balance between two forces: brands, which compete for value, and retailers, who compete for price, mainly in commodities. PL already exceeds 53% of market share in Spain according to Kantar.

Following his explanation, markets where there is a balance between the two forces add value to the consumer and grow in the long term, but this does not happen in his opinion in Spain: "The growing power of operators that prioritize price is unbalancing the consumer market, with growing assortments of PL and less brands and innovation, which decisively conditions the choice of the consumer and therefore the KPIs of the market".

THE ASSORTMENT DETERMINES THE BASKET According to data from Kantar Worldpanel, the sum of six main chains, PL has gone from 2018 to 2022% share in the period 46-53. It maintains constant growth, especially important in periods of crisis, pushing down prices. The evolution of the value in packaged products for the period 2001-2019 was 59.8% (the volume increased by 23.6% and the net value by 36.2%). If we take into account inflation at this time, of 47.6%, it is concluded that there has been a loss of value of -11.4%. "Large consumption does not grow at the pace of inflation and has eroded in value," says Valencoso. With regard to the number of innovations, these have fallen by 38% in the period 2011-2021. The consumer's basket is absolutely conditioned by the assortment, says Valencoso. In fact, taking 2021 data as a reference, Mercadona customers, who buy 67.8% in PL products, when they go to Carrefour only spend 22.7% on own-brand items; 75.2 per cent in Lidl; and 18.3%, for example, in Eroski. On the other hand, if the weight of the PL in Lidl is 77.9%, its customers spend 71.1% on their own brand when they buy in Mercadona; 24.5% in Carrefour; and 23.7% in Eroski. THE AUTHORITIES' GROWING INTEREST IN RETAIL ALLIANCES In a later block, Javier Berasategi, expert lawyer in Competition and Regulation of the Food Chain, has placed the focus on retail alliances in the conference organized by Promarca, highlighting the growing interest in this point of the competition authorities. They are very dynamic structures, which overlap and with constant entries and departures of partners. They are alliances that are created and closed, accumulating in this process great confidential information. Its objectives are varied, such as the joint purchase of PL and A-brands, and the provision of services. On this last point, Berasategi believes that many of these services are not such or are charged at exorbitant prices, sometimes even for the mere fact of meeting...

In short, these are the international alliances that provide services:

Coopernic (2006), which brings together Coop, Ahold Delhaize, Leclerc and Rewe

Agecore (2015), with Colruyt, Edeka, Intermarché, Conad, Coop and Eroski

Eurelec (2016), with Leclerc and Rewe

Horizon Int. Services (HIS) (2019), with Auchan, Casino, Metro and Dia

This Competition expert has highlighted the creation in 2022 by the French Parliament of an investigative commission on distributor alliances, which verified the access toll that the agreement with the alliance entails, without which there is no negotiation or national agreement; the absence of tangible services (“fictitious services”) or charged at disproportionate prices; the impossibility of contracting these services; the dereferencing or cessation of massive purchases by partners to force an agreement with the alliance; and the leak of confidential information between alliances. Likewise, the possible avoidance of the French regulatory and tax framework was questioned.

In relation to the regulations for the Defense of Competition, he has cited the case of four alliances:

Centrale Italiana (ITA, 2014), which accounted for 23% of purchases and more than 40% in local sales markets, which was dissolved after an agreement with the authority.

Dia / Eroski (ES, 2016), where the complaint was filed by the CNMC, although the appeal is pending.

Casino / Intermarché (EU, 2019), whose inspection was annulled by the CJEU

Carrefour / Povera (BE, 2021), with 20-25% of the market.

The file was archived by agreement: legally separate purchasing function, limited exchange of information, negotiation of financial discounts with no impact on the commercial strategy of distributors.

Regarding the regulation of the food chain, Javier Berasategi has referred to the Dia / Eroski affair, in his opinion a very solid precedent to stop the abuses of distributor alliances and which ended with sanctions worth 6.8 million euros, having a sentence of the Central Court of "acquittal" to Eroski in 2019; and, on the other hand, a sentence of the National Court of "condemnation" of Dia in 2020 and another of the Supreme Court in the same sense in 2021.

Regarding the future, he has spoken about the revision of directive (EU) 2019/633, which will be evaluated before 2025 and could be the Achilles heel of alliances. He will have to see the interpretation that is made of the prohibition of "commercial retaliation" and "payments not related to the sale of the products" in the Member States. He remains to see if linking services to purchase agreements will be prohibited. ROUND TABLE ON THE IMPORTANCE OF VALUE CREATION

The Promarca conference closed with a round table on the importance of creating value, with the participation of Javier Alejandre, a UPA technician; Álvaro Areta, COAG technician; Gabriel Trenzado, general director of Cooperativas Agroalimentarias; and Mauricio García de Quevedo, general director of FIAB.

For Álvaro Areta, a COAG technician, the chain must provide sufficient value for its own sustainability: "The challenge is to obtain a decent income for the links, because, despite the fact that agriculture is going very well and that 2022 has been a record year, the people who are part of this sector are not doing so well.”

Given that the first link is already very transparent with its sales prices, Areta sees it essential that the observatories function and publish studies on those of the rest of the links, so that Spanish law is an example for the rest of the EU Member States. "That Juan Roig recognizes that they are capable of destroying a sector if prices do not rise is important for it to be known," he adds.

Very accurate in his analysis, Gabriel Trenzado, general director of Cooperativas Agroalimentarias, in making clear that in the food chain there is a value that nobody pays: "We have seen how sensitive the consumer and the public authorities themselves are to the rise in prices... That It doesn't happen in other sectors.

Javier Alejandre, a UPA technician, notes that, in 2022, farmers and ranchers lost 5.5% of gross income. However, for him, the law of the food chain is a useful tool: "It is probably an excessively regulated sector, but this law is basic." Gabriel Trenzado, general director of Cooperativas Agroalimentarias, points out a factor that cannot be ignored: drought and other factors are affecting production. "Not everyone has lost: those who have had product have done well," he says. For Trenzado, transparency is key, that dynamic market studies can be done for the knowledge of the links: "That is not only looked at at the production level but also at the PVP level". The law of the food chain, rather than generating value, creates the conditions for greater legal certainty, but "it will not balance the forces, because that is achieved with other instruments and structuring the sector is not done via decree," he concludes. For Mauricio García de Quevedo, CEO of Fiab, the current hyperregulation has high associated costs: "With more taxes and more regulatory costs, such as the plastic tax, the profitability of the company is eroded, because all those costs cannot be imputed in consumer prices." According to their data, the situation is complex in the industry: if the average profitability is 8.32%, last year it fell to 7%.

In summary, the fall in profitability has three causes for the Fiab representative:

Shortage in the supply of inputs and raw materials.

Increasing the impact of energy costs. From 8% on average to an impact of 25-30%

Over-regulation, which erodes margins and produces inflation.

Asked about the law of the food chain, García de Quevedo emphasizes that it generates a great value to the balance in commercial relations: "It regulates abuses and black practices; Likewise, including selling at a loss is a great advance, as well as regulating promotional activities and that associations can appear to report abuses. "

See here for more: Manufacturer brands, in the face of the MDD tsunami (foodretail.es)

This shift toward private labels is especially clear in the skin care industry, where high-quality private label skincare and private label cosmetics are now matching—or even exceeding—big-name brands in performance and appeal. At Made by Nature Labs, we’ve seen firsthand how customized, clean-label formulations empower businesses to build strong brand identities. As value and innovation take center stage, private labels are reshaping the beauty market.