Research: Discount Channels Emerge as Primary Drivers of Private Label Growth

- DRC Discount Retail Consulting GmbH

- Apr 27

- 2 min read

Updated: Apr 29

Data from Circana signals a structural shift in global retail: private label growth is no longer just incremental — it is being propelled by value-driven channels like discounters and club stores. As inflation and squeezed purchasing power persist, own brands have evolved from "budget alternatives" into core strategic assets that drive loyalty and margin.

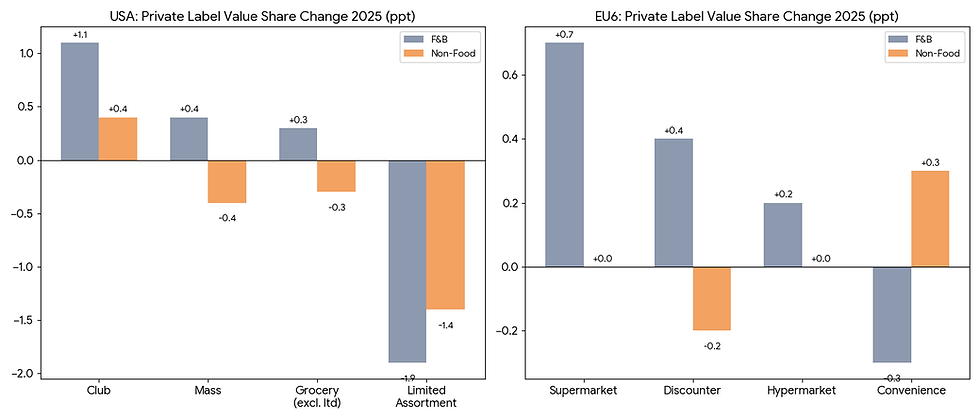

The US Market: The Rise of the Club Format

In the United States, private labels have reached a massive $330 billion valuation, securing over 20% of the market share.

The Growth Engine: Nearly half of all private label growth is driven by club formats, as consumers prioritize bulk value.

Market Shift: Mass and club channels are capturing the lion's share of gains, while traditional grocery stores face more volatile performance.

The European Market (EU6): A Volume Powerhouse

The shift is even more aggressive in Europe, where private labels have hit an all-time high of 50% volume share.

Supermarkets vs. Discounters: While traditional supermarkets remain the largest contributors by volume, discounters are the primary growth accelerators.

Price Leadership: Discounters are increasingly acting as the market's "price setters," forcing traditional retailers to adapt.

Strategic Takeaways

The evolution of private labels can be summarized into three core shifts:

Channel Migration: Growth is concentrated in value-oriented channels (discounters and club stores) rather than traditional retail formats.

Perception Flip: Own brands have moved beyond the "cheap substitute" labels. They now compete directly with national brands on innovation, quality, and consumer trust.

Macro-Catalysts: Sustained inflation remains the primary driver, turning private label strategy from a tactical response into a long-term pillar of retail survival.

Conclusion

To maintain momentum, retailers must pursue a dual-track strategy: continue capturing market share through value-tier products while simultaneously scaling premium private label offerings to compete at the high end.

Source: Circana, 2026

Comments